Understand the Basics of Budgeting

Familiarize yourself with budgets. A budget is like a roadmap for your business — it provides an overview of what you will be spending and making over a future time period. A proper budget will include educated estimates as to what you will make (revenues), and a precise plan for your spending. Following your budget successfully can ensure your business is profitable and achieves its goals. For example, assume your business is planning for next year. A budget will outline your estimated revenues, and then include a plan for expenses that is less than those revenues, so that you can earn a profit. A balanced budget means your revenues are equal to your expenses. A surplus means your revenues exceed expenses, and a deficit means expenses exceed revenues. As a business, your budget should always strive to be in a surplus state.

Learn why budgeting is essential. A well-formed budget is essential to the success of your business because it allows you to match what you spend to what you earn. Without a clear plan for your spending, it is very easy to outspend your revenues over time, which can lead to losses, increases in debt, and the potential closure of your business. A budget should guide every single business expenditure. For example, if you realize midway through a year that your business desperately needs updated computers, you can consult your budget to see how much estimated surplus revenue you will generate for the remainder of the year. You can then explore costs for computer upgrades and see if that fits within the surplus figure while allowing you to earn a profit, or alternatively, if you have the additional revenue to support taking out a loan for the computers. A budget can also help you see if you are spending too much, and need to make cuts midway through the year.

Familiarize yourself with each component of a budget. There are three basic components to a business budget, according to the Small Business Administration. These are sales (also known as revenues), total costs/expenses, and profits. Sales: Sales refer to how much total money your business brings in from all sources. A budget will involve an estimate or forecast of your future sales. Total costs: Total costs are what it costs your business to generate your sales. These include fixed costs (like rent), variable costs (like materials used to make your products), and semi-variable costs (like salaries). Profits: Profits are equal to revenues minus total costs. Since profit is the goal of business, your budget should include expenses that are low enough to earn you a decent return on your investment.

Forecasting Revenue

Consider your current position. If you are a business with a few years of operations, your revenue forecasting process will involve examining previous years' revenues and making adjustments for the upcoming year. If you are a new startup with no business experience, you will need to estimate your total sales, price per product, and do market research to see what a business of your size can expect to earn. Remember that revenue forecasts are rarely accurate. The point is to provide the best possible estimate using the knowledge you have. Always be conservative. This means assume you will receive sales volumes and pricing on the low end of the possible range.

Perform market research to determine pricing. This is especially important for new businesses. Examine businesses in your region that provide similar goods or services. Take note of the prices of their products or services. For example, assume you are opening a therapy practice. Therapists in your region may charge $100 to $200 per hour. Compare your qualifications, experience, and service offerings to your competition, and estimate your price. You may decide $100 is wise. If you offer multiple products and services, make sure to research prices for those too.

Estimate your sales volumes. Sales volumes are how much of your product you sell. Your revenues are equal to your price per good/service multiplied by the number of goods or services you provide. You will therefore need to estimate how much of your good/service you will sell over the course of the year. Do you have any customers or contracts lined up? If so, include these. You can then assume referrals from customers and advertising will add to these volumes over the year. Compare to existing businesses. If you have colleagues who have established businesses, ask them what their volumes were like early on. For a therapy practice, your colleagues may tell you during their first year they averaged about 10 client hours a week. Look at what drives sales volumes. If you are opening a therapy practice, for example, your reputation, referrals, and advertising will bring in people. You could decide that based on these resources, one new client every two weeks is reasonable. You could then go further and make an estimate that each client will pay for one hour a week, and last for an average of six months. Once again, remember that revenue forecasts are purely estimates.

Use past data. This is essential if you are a well established business. One effective strategy for forecasting is to take the previous year's revenue, and then examine what changes will occur over the next year. Look at pricing. Do you have reason to believe your prices will increase or decrease? Look at volume. Are more people going to be purchasing your product or service? If your business has been growing by 2% annually, you can assume the same for the following year if no significant changes have occurred. If you plan on aggressively advertising, you could bump that up to 3%. Look at the market. Is your market growing? For example, imagine that you run a coffee shop in a downtown neighborhood. You may be aware that the neighborhood is rapidly growing due to new people moving in. This could be reason to add to your growth forecast.

Creating the Budget

Get a template online. The best way to start creating a budget is by getting a template online. A template will have all the available information, and your job will simply be to fill in the spaces with your estimates. This prevents you from needing to spend time building complex spreadsheets. Contact an accountant if you are having difficulties. Chartered Professional Accountants in the UK and Certified Public Accountants (CPAs) in the US are trained to advise businesses in the area of budgeting, and for a fee they can assist you in any aspect of the budget creation process. A simple online search of "business budget template" can yield thousands of results. You can even find custom templates for your particular type of business.

Decide on your target profit margin. Your profit margin will be equal to your revenues minus your total expenses. For example, if your business is estimated to have $100,000 in sales, and total expenses of $90,000, you will have a $10,000 profit. This would equal to a 10% profit margin. Research online or ask a financial adviser what the typical margins for your kind of business should be. If 10% is typical for your business, you know that if you are forecasting $100,000 of revenues, your expenses should equal no more than $90,000.

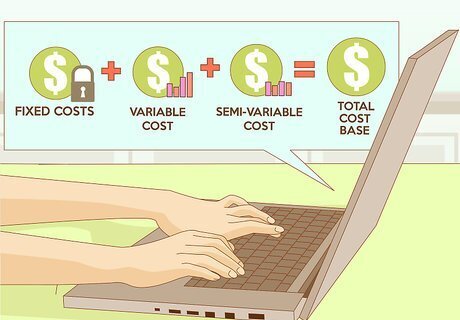

Determine your fixed costs. Fixed costs are costs that generally remain the same throughout the year, and they include things like rent, insurance, and property taxes. Add up all these costs to get an idea of your fixed costs for the next year. If you have past financial data, use these fixed costs and adjust them for any rent increases, bill increases, or new costs.

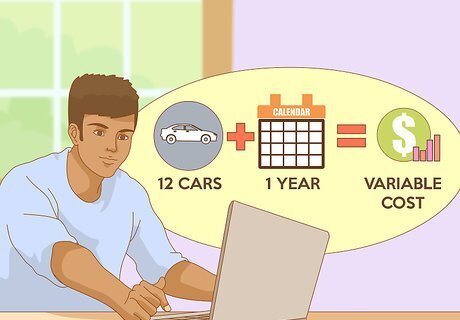

Estimate your variable costs. The cost of raw materials and inventory to make your sales is the key variable cost. For example, if you are a car dealership, this would include inventory you purchase and sell every year. This will vary depending on how much you sell, which is why it is known as a variable cost. You can use your revenue forecast to determine this. For example, if you estimate you will sell 12 cars in your first year, your inventory costs will be the cost to purchase 12 cars.

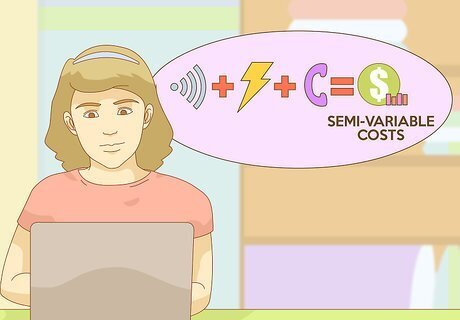

Estimate your semi-variable costs. These are expenses that usually have a fixed component, but also vary depending on activity. For example, telephone or internet data packages have a set cost plus any overage for usage. Salaries are also an example. You may have a forecasted salary for an employee, but overtime or extra hours due to extra work could raise this cost. Add up all your estimated semi-variable costs.

Add the three types of costs together and make adjustments. Once you have a total for each type of cost, add them together. This will be your total cost base for the year. You can then ask yourself some key questions. Are your total costs less than your revenues? Do your total costs provide a profit margin greater than or equal to your target? If the answer to either of these questions are no, you will need to look into making cuts. To do this, look at all your costs, and examine what you can do without. Labor costs are one of the most flexible areas to find savings (though you risk upsetting your employees when you cut hours). You can also look into finding a location with lower rents, or reducing utilities costs.

Comments

0 comment