X

Research source

How exactly these events are recorded is relatively simple, but depends largely on the type of dividend being issued.

Cash Dividends

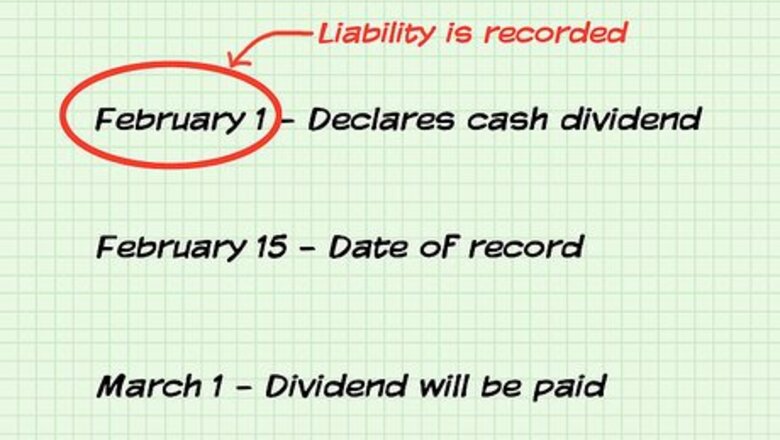

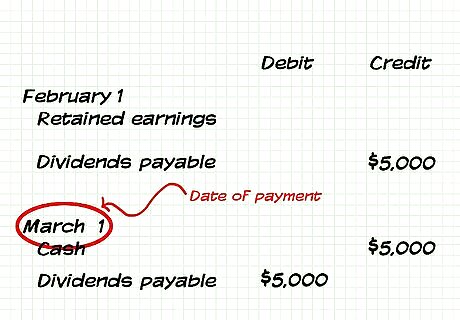

Recognize when to record the liability of the company to pay the cash dividends. This occurs on the "date of declaration," when the board of directors formally authorizes payment of dividends. Under standard accounting procedures, expenses are recorded when they are incurred. In this case, dividend expenses are recorded because by declaring them the company is held liable to make good on the declaration and deliver the dividend. A declaration specifies when the declaration is made, when the date of record is, and when the dividend will be paid. The date of record specifies the date by which a shareholder must own stock in order to qualify for the dividend. For example, imagine your company declares a cash dividend on February 1 that will be paid to shareholders on March 1 and that the date of record is set at February 15. The liability would be recorded on February 1.

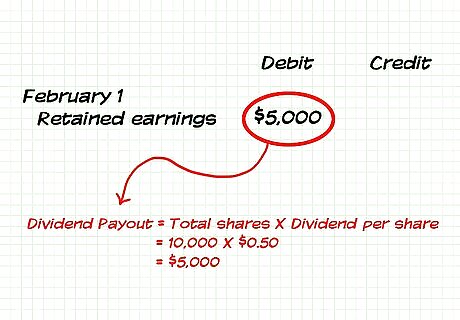

Debit the retained earnings account. Debit the retained earnings account for the total amount of the dividends that will be paid out. This will function as a decrease in this account because money that could have been retained is being paid out instead. This entry is made on the date of declaration. Continuing the previous example, imagine you company has 10,000 shares outstanding (total shares) and decides to issue a dividend of $0.50 per share. Your total debit from retained earning would be the same as the total value of the dividend payout, or $5,000 ($0.50 x $10,000).

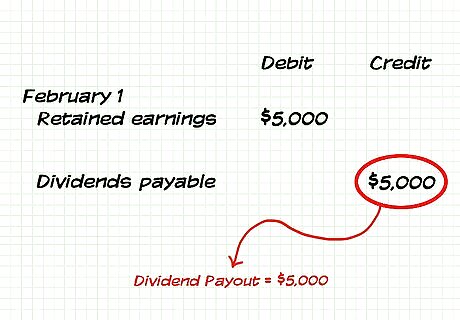

Credit the dividends payable account. The dividends payable account recorded how much the company owes to shareholders between declaring a dividend and actually paying it. This account will be credited (increased) on the date of declaration. Like the debit to retained earnings, the amount credited will be the total value of the dividends declared. In our example, your company would credit dividends payable for $5,000 (the same amount as was debited from retained earnings).

Record the transaction on the date of payment. The only other entry needed when issuing a cash dividend is the entry on the date on which the company actually pays the cash dividend. Because this is a cash payment, you would credit the cash account (decreasing it) and debit the dividends payable account (decreasing it). This is because both transactions represent money leaving the company. Again, the value recorded will be the total value of the dividends paid. So, in our example, you would credit cash for $5,000 and also debit dividends payable for $5,000 on the date of payment, March 1.

See the big picture. When you declare and pay a dividend, the transaction will affect your company's balance sheet. At the end of the account period, you'll be left with a cash account and retained earnings account that are lowered by the amount of the dividend that you paid out.

Stock Dividends

Understand stock dividends. A stock dividend is another type of dividend that doesn't involve the distribution of any cash to shareholders. Rather, a stock dividend distributes additional shares of the company to shareholders, perhaps at a percentage rate to shares that they already hold. Though this will increase the total number of shares outstanding, it does not transfer more money to shareholders or away from the company. Instead, it simply dilutes the value of shares and transfers money between retained earnings and shareholder equity.

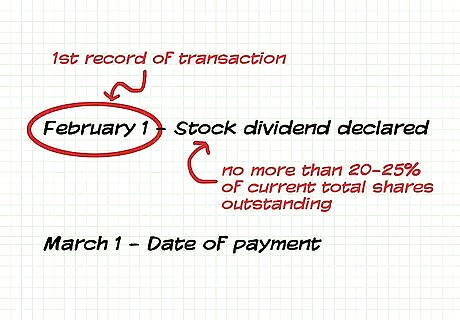

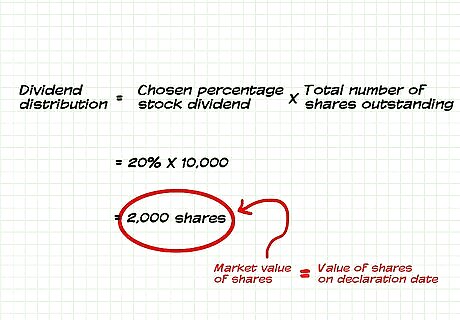

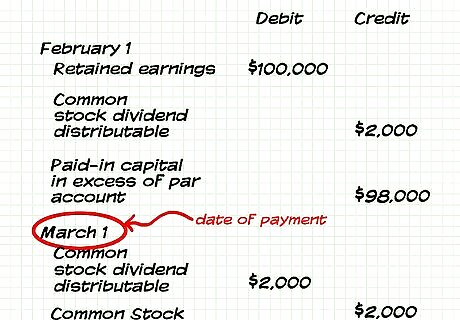

Know when to recognize a stock dividend. Just like a cash dividend, a stock dividend will be declared on a specific date and will offer a specific number of shares to be distributed. Generally, a stock dividend will be made for an increase of no more than 20-25% of current total shares outstanding. This is because anything more would be categorized differently, as a a stock split (a dilution of shares to manipulate market price). For example, your company may declare on February 1 to issue a 20% stock dividend on your 10,000 outstanding shares on March 1, the date of payment. February 1 would mark the first recording of this transaction.

Find the value of the dividend distribution. Multiply the number of shares to be distributed by the market value of each share. This amount is one of the values that you will record in the following steps and represents the total book value of the stock dividend distribution. The number of shares distributed will simply be the chosen percentage stock dividend (20% in our example) multiplied by the number of shares outstanding. In the example, this would be 10,000 x 20%, or 2,000 shares. The market value of each share used should be the value that a share of the company trades for on the declaration date.

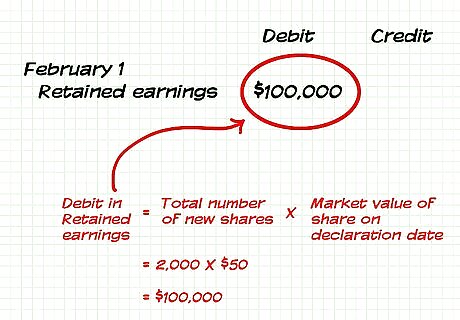

Debit the retained earnings account. The retained earnings account should be debited (decreased) by the amount found in the last step (the market value of shares x the number of new shares). This entry should be posted on the declaration day. To continue our example, imagine that the market value of a share of your company is trading for $50 on the declaration date. Then, the amount debited from retained earnings would be $50 x 2,000, or $100,000.

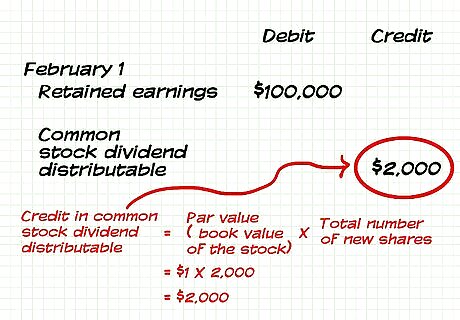

Credit the common stock dividend distributable account. This account will be credited by an amount defined by the number of shares distributed times the par value of the stock. The par value here is the book value of the stock and should already be recorded in any company's books. This entry should be posted on the declaration day. Imagine that for our example the par value is $1 per share. Thus, the amount credit to the common stock dividend distributable account would be $1 x 2,000 shares, or $2,000.

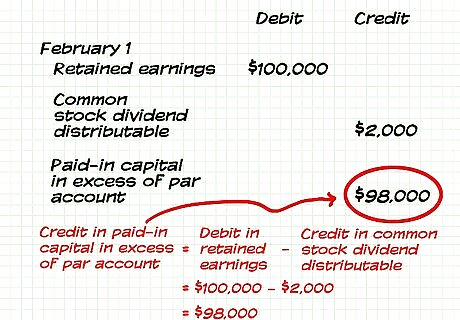

Credit the paid-in capital in excess of par account. This account will be credited by an amount defined by the difference between the amount debited from retained earnings and the amount credited to common stock dividends distributable. This account represent the amount of money distributed above and beyond the par value of the stock. This entry should be posted on the declaration day. In our example, this amount would be $100,000 (the amount debited to retained earnings) minus $2,000 (the amount credited to common stock dividends distributable), or $98,000.

Record the payment of the stock dividends. On the date of payment (when the shares are distributed to shareholders), another accounting entry must be made. This is done by debiting the common stock dividends distributable account and crediting the common stock account by the same amount. This amount will be the amount previously credited to the common stock dividends distributable account. In the example, your debit and the credit amounts for this entry would be $2,000.

Comments

0 comment