Checking If You Can Remove the Account

Obtain a free credit report. You are entitled to one free credit report from Equifax each year. You shouldn’t request it directly from Equifax. Instead, you can request a report in the following ways: Call 1-877-322-8228. Visit http://www.annualcreditreport.com and enter your information. You can get a copy of your report immediately. Fill out the Annual Credit Report Request Form available at https://www.consumer.ftc.gov/sites/www.consumer.ftc.gov/files/articles/pdf/pdf-0093-annual-report-request-form.pdf. Mail the completed form to the address printed on the form.

Check if any accounts are not yours. You want your credit report to be accurate. To that end, you should go through and identify any errors. Highlight any credit accounts that don’t belong to you. Also highlight any other errors you see. You can report all mistakes at the same time.

Identify the age of a closed account. You might have closed an account in the past. This situation is different than if the credit account was never yours to begin with. You can have closed accounts removed after a certain amount of time has passed: An account that was closed but in good standing can stay on your credit report for up to 10 years. If the credit information is positive, you might want to leave it on your report. A delinquent account that was charged off will remain on your report for seven years plus 180 days from the point you became delinquent. An account in collections will remain on your account for seven years plus 180 days from the date it became delinquent. Also, an account in collections may show up twice on your credit report. It may show up once for delinquency and once for collection.

Asking Equifax to Remove the Account

Contact Equifax online. Visit their website at https://www.equifax.com/personal/. Click on “Credit Report Assistance” and then “Dispute Info on Your Credit Report.” You can submit your information online.

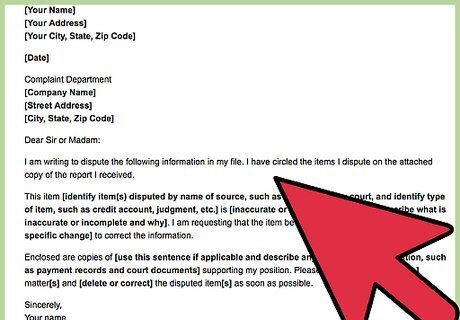

Write a letter. Even if you report online, you should also write a letter, which will serve as evidence of your communication. In your letter, you should identify the closed credit account and ask that it be removed. Also explain why it should be removed, e.g., you never opened the account or it is so old it should have fallen off the report by now. You can use the Federal Trade Commission’s sample letter, which is available at https://www.consumer.ftc.gov/articles/0384-sample-letter-disputing-errors-your-credit-report.

Mail the letter. Make a copy of the letter for your records. Make copies of any attachments, such as the copy of your Equifax credit report. Mail the letter certified mail, return receipt requested. Equifax’s mailing address is Equifax Information Services, LLC, P.O. Box 740256, Atlanta, GA 30348.

Receive the results of the investigation. After Equifax receives your complaint, it will contact the entity that reported your credit account and ask them to investigate. Equifax must get back to you within 30-45 days. Equifax should explain in writing the results of the investigation. Equifax should also send you the identity and contact information for the entity that reported the account.

Write a statement of dispute, if necessary. If Equifax won’t remove the closed account, then you can write a statement of dispute for free. This statement will be included whenever someone requests your Equifax credit report. Generally, you should only include a statement of dispute if you have legitimate reasons for disagreeing with Equifax’s decision not to remove the account. For example, you could write, “I never opened this account though Equifax refuses to remove it from my credit history. I am investigating whether I was the victim of identity theft.”

Having a Creditor Remove the Account

Send a letter to the creditor. You can ask the entity that reported the credit account to remove it. You should write them a letter and mail it certified mail, return receipt requested. Equifax should have given you the contact information for the entity. Remember to include a copy of your Equifax report with the credit account highlighted or circled. The FTC also has a helpful sample letter you can use: https://www.consumer.ftc.gov/articles/0485-sample-letter-disputing-errors-your-credit-report-information-providers. Tailor the FTC letter to your situation. If you never opened the account, then ask that it be removed. However, if the account was closed because you were delinquent, then you can explain why you were unable to pay your bills and ask for a good faith deletion. If you are asking for a good faith deletion, then keep your tone courteous. Remember, the creditor doesn’t have to remove the closed account information.

Be careful about negotiating. A creditor or collections agency might want to negotiate with you after you contact them. For example, they might agree to take the negative information off your account if you agree to make payment. This is called “pay for delete.” Be careful. By agreeing to pay, you might re-start the debt. For example, a collections account should fall off your credit report after seven years. If the account is six years old, it should fall off in a year. By agreeing to start making payments, however, the account becomes new—it is now zero years old. If you can’t make all of your payments, the creditor will back out of deleting the account, and it won’t fall off for seven more years.

Meet with a lawyer if you want to negotiate. Your delinquent account might only be one or two years old. In this situation, you might want to negotiate because the account won’t fall off for five or more years. However, before talking with the creditor, you should meet with a lawyer to get advice. You can reach a lawyer by contacting your local or state bar association and asking for a referral. If you are low income, then look into legal aid, which provides legal help for free or for a reduced price. You can find legal aid by visiting http://www.lsc.gov.

Continue to monitor your credit report. If the creditor agrees to remove the closed account, then continue to monitor your Equifax account. Although you only get one free credit report a year, you could still sign up for credit monitoring with Equifax for $19.95 a month.

Comments

0 comment